Cerebras is redefining AI hardware with wafer-scale computing, challenging GPU clusters and reshaping the future of AI infrastructure.

Cerebras Systems is heading toward one of the most closely watched semiconductor IPOs of the AI era, with plans to list on Nasdaq under the ticker CBRS. The company sits at the intersection of breakthrough chip design, extreme performance claims, and equally extreme execution risk. At a time when Nvidia dominates AI hardware, Cerebras is trying to convince investors that a radically different architecture—wafer-scale computing—can carve out a meaningful share of the market.

The IPO is being discussed at a valuation of roughly $22–$25 billion, with expectations of raising around $2 billion. That would immediately place Cerebras among the largest semiconductor listings in history. But the real question for investors is not size—it’s whether the company can turn its unconventional technology into durable, diversified revenue beyond a small set of hyperscale customers.

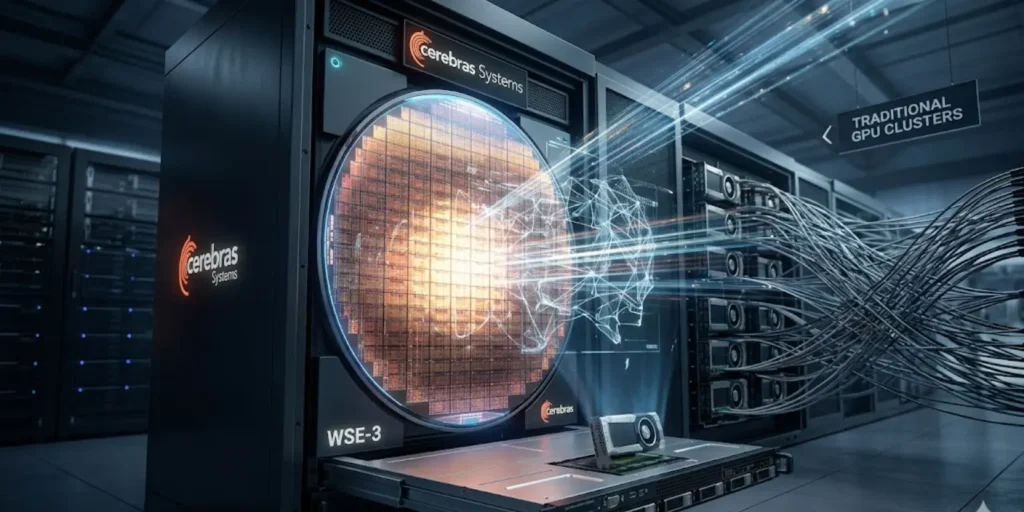

The Core Idea: Replacing GPU Clusters With a Single Giant Chip

At the heart of Cerebras is a simple but aggressive bet: modern AI systems are bottlenecked less by raw compute and more by data movement between chips. Traditional AI infrastructure relies on thousands of GPUs linked together, constantly transferring data across networks. That communication overhead creates latency, power inefficiency, and engineering complexity.

Cerebras replaces that entire model with a wafer-scale chip called the WSE-3, which is built from an entire silicon wafer rather than being cut into smaller dies. This design packs trillions of transistors into a single unit and connects them using on-chip fabric instead of external networking. The result is a system that, in theory, eliminates most inter-chip communication delays.

This architecture allows Cerebras to claim massive advantages in training large AI models, particularly those requiring trillions of parameters. Instead of distributing workloads across thousands of GPUs, the company argues it can run them on a single integrated system with fewer engineering layers and lower energy overhead.

The Technology: WSE-3 and the Promise of Wafer-Scale AI

The current-generation WSE-3 chip is the centerpiece of Cerebras’s IPO narrative. It is physically enormous by semiconductor standards and contains an estimated 4 trillion transistors and 900,000 compute cores. The company positions it as one of the most powerful AI chips ever built, optimized specifically for large-scale training and inference workloads.

What makes this approach unusual is not just scale but philosophy. While Nvidia and AMD focus on modular GPUs that can be stacked into clusters, Cerebras eliminates the cluster concept. Instead of scaling horizontally with more chips, it scales vertically by increasing the capability of a single wafer.

In practical terms, this means fewer software layers, less distributed systems complexity, and potentially faster iteration cycles for AI developers. However, it also introduces manufacturing risk, yield challenges, and a reliance on extremely advanced fabrication processes that only a few foundries can support.

The OpenAI Deal: A Turning Point or a Risk Concentration?

One of the most important developments ahead of the IPO is Cerebras’s reported $10 billion compute agreement with OpenAI. This contract instantly changes how investors evaluate the company because it shifts Cerebras from a niche hardware experiment into a strategic infrastructure partner for the world’s leading AI lab.

The deal is expected to span multiple years and support massive compute capacity expansion for training and inference workloads. If fully realized, it could account for a significant portion of Cerebras’s future revenue and help validate its wafer-scale architecture at real-world scale.

However, the same deal introduces concentration risk. Rather than relying heavily on one legacy customer, Cerebras is now heavily exposed to OpenAI’s execution roadmap and capital spending cycle. If demand assumptions change or deployment timelines slip, revenue visibility could weaken quickly.

The Business Reality: Fast Growth, Small Base, High Dependency

Cerebras is still early in its commercial life cycle. Revenue is estimated in the low hundreds of millions annually, which is tiny compared to established semiconductor giants. Yet the company has reported extremely high year-over-year growth rates, driven by early adoption from AI labs and government-linked customers.

The most concerning structural issue is customer concentration. Historically, a large share of revenue came from a single Middle Eastern technology customer. While this dependency is expected to decline with OpenAI’s entry, the company is still far from having a diversified enterprise base.

This creates a classic IPO tension: explosive growth potential on one side, and fragile revenue structure on the other. Investors are essentially being asked to price in a future where Cerebras becomes a mainstream AI infrastructure provider, not a niche specialist.

The Competitive Landscape: Nvidia Still Sets the Rules

Even with its technological ambition, Cerebras is entering a market dominated by Nvidia. NVIDIA’s advantage is not just hardware performance but ecosystem lock-in. Its CUDA software platform has become the default development environment for AI workloads, deeply embedded across research labs, startups, and enterprise systems.

Cerebras does not directly compete on compatibility. Instead, it targets specific workloads where wafer-scale architecture may outperform GPU clusters—especially large model training and high-efficiency inference. This is a narrower but potentially high-value segment of the market.

The challenge is adoption friction. Switching away from Nvidia requires retraining infrastructure, rewriting workflows, and accepting a less mature software ecosystem. That creates a high barrier for Cerebras to expand beyond early adopters.

IPO Valuation: Growth Justification vs. Reality Check

At a potential valuation of $22–$25 billion, Cerebras would be priced at an extremely high revenue multiple for a semiconductor company. That premium reflects expectations of rapid scaling, strategic importance in AI infrastructure, and successful expansion of its customer base.

The bullish argument is straightforward: if AI compute demand continues to grow exponentially, and wafer-scale computing proves efficient at scale, Cerebras could capture a meaningful slice of a multi-hundred-billion-dollar market. In that scenario, today’s valuation could look conservative in hindsight.

The bearish perspective is equally clear: the company is early, unprofitable, highly concentrated in a few customers, and competing against one of the strongest technology monopolies in modern computing history. Any slowdown in growth or delay in adoption could compress valuation sharply.

How Investors Can Approach the IPO

For most retail investors, the simplest path will be waiting for the public listing on Nasdaq under CBRS. Pre-IPO access is limited and typically restricted to accredited investors through secondary markets, which carry liquidity constraints and pricing uncertainty.

Once the stock begins trading, volatility is expected. Semiconductor IPOs tied to AI narratives often experience sharp early swings as institutional positioning adjusts and lock-up periods approach expiration. Many investors wait for post-IPO stabilization or initial earnings clarity before building positions.

A more conservative approach is indirect exposure through semiconductor ETFs or diversified AI infrastructure funds, which may later include Cerebras if it achieves sufficient scale and liquidity.

Final Perspective: High Risk, High Conviction Story

Cerebras is not a typical semiconductor IPO. It is a bet on whether AI infrastructure can move beyond GPU clusters into fundamentally new compute architectures. The company has real technological innovation, credible institutional backing, and a landmark OpenAI contract that gives it legitimacy in the most important AI market on earth.

But it also carries significant uncertainty. Customer concentration, manufacturing dependency, and ecosystem maturity are all unresolved challenges. The IPO will likely price somewhere between optimism and skepticism, and the market will quickly test whether the story is ahead of—or aligned with—reality.

For investors, Cerebras represents a classic frontier technology trade: potentially transformative upside paired with execution risk that cannot be ignored.